Bookkeeping 101: A Comprehensive, Practical Guide for Business Owners

If you run a business, bookkeeping is not optional—it is foundational. Whether you are a solopreneur, consultant, creative, or owner of a growing small business, bookkeeping is the system that allows you to understand what is actually happening financially inside your business. Without it, decision-making becomes guesswork, tax season becomes stressful, and growth becomes riskier than it needs to be.

This guide is an expanded, in‑depth version of my Bookkeeping 101 webinar, written for business owners who want clarity without jargon and structure without overwhelm. You do not need to be good at math, and you do not need an accounting background. What you do need is an understanding of how bookkeeping works, why it matters, and how to approach it responsibly—either on your own or with professional support.

By the end of this article, you will understand the purpose of bookkeeping, the accounting principles behind it, the most important bookkeeping tasks, how to build a sustainable routine, how to choose software like QuickBooks or Wave, and when it makes sense to hire help.

If you prefer video: This article is based on my full Bookkeeping 101 webinar. You can watch the complete session on YouTube for a guided, visual walkthrough of these concepts.

Why Bookkeeping Matters More Than Most Business Owners Realize

At its core, bookkeeping has one primary purpose: it produces financial reports you can trust. These reports tell you where your business actually stands—not what your bank balance feels like, not what you hope is happening, but what is objectively true.

Many business owners rely on their bank account balance as a proxy for financial health. Unfortunately, this is one of the fastest ways to misunderstand your business. Your bank balance does not account for unpaid bills, upcoming tax obligations, customer invoices that have not yet been paid, or long‑term liabilities like loans.

Accurate bookkeeping allows you to prepare properly for taxes, including income tax, payroll tax, and sales tax. It reduces the likelihood of surprise tax bills and penalties, and it allows tax filing to be smoother and less stressful. When your books are consistently maintained, your tax professional can focus on strategy rather than cleanup.

Bookkeeping also provides the data you need to evaluate profitability. It shows whether your business is improving over time or quietly struggling. It helps you identify expenses that are draining resources without providing a justifiable return. It allows you to spot trends early rather than reacting too late.

Finally, clean books are essential for credibility. Banks, lenders, landlords, investors, and even potential partners will ask for financial reports. When you can produce them quickly and confidently, you position yourself as organized, responsible, and trustworthy.

Good bookkeeping does not guarantee success—but bad bookkeeping guarantees uncertainty.

Bookkeeping vs. Accounting: Clearing Up a Common Confusion

Bookkeeping and accounting are closely related, but they are not the same thing.

Bookkeeping is the process of recording, organizing, and maintaining financial activity. It is concerned with accuracy, consistency, and structure. Accounting is the interpretation and analysis of that information. Accounting uses financial reports to assess performance, ensure compliance, and support decision‑making.

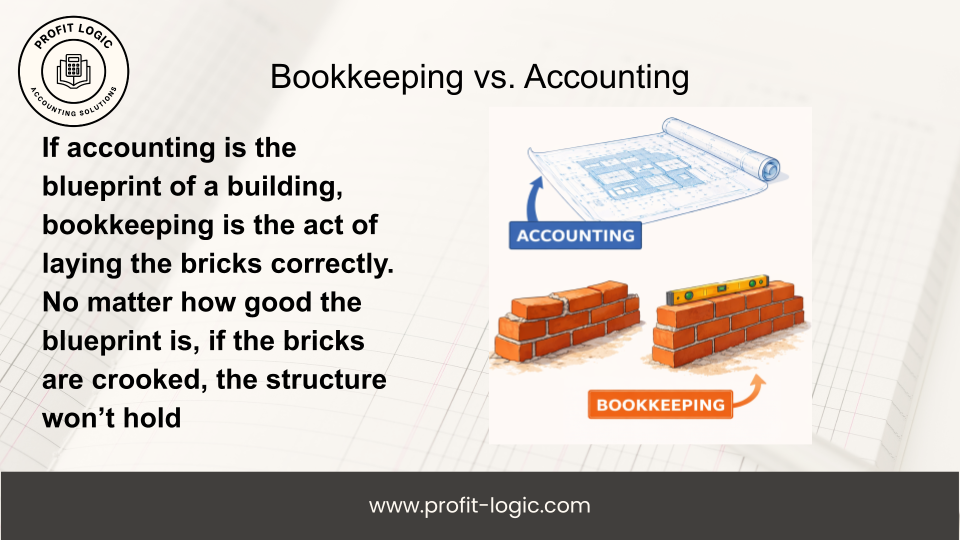

A helpful analogy is this: if accounting is the blueprint of a building, bookkeeping is the act of laying the bricks correctly. No matter how good the blueprint is, if the bricks are crooked, the structure will not hold.

This distinction matters because many software tools blur the line between bookkeeping and accounting. While software can automate parts of the process, it cannot think critically. If transactions are categorized incorrectly, the resulting reports will still be wrong—even if they look polished.

This is why fundamentals matter. Today’s session—and this article—focuses on structure, not shortcuts.

The Foundation of Modern Bookkeeping: Double‑Entry Accounting

Nearly all professional bookkeeping systems rely on double‑entry accounting. This system ensures that every financial transaction affects at least two accounts. When money moves, something is gained and something is given up.

For example, when a client pays you for services, your cash increases and your revenue increases. When you purchase software for your business, your cash decreases and your expenses increase. Each transaction has two sides, and both must be recorded correctly.

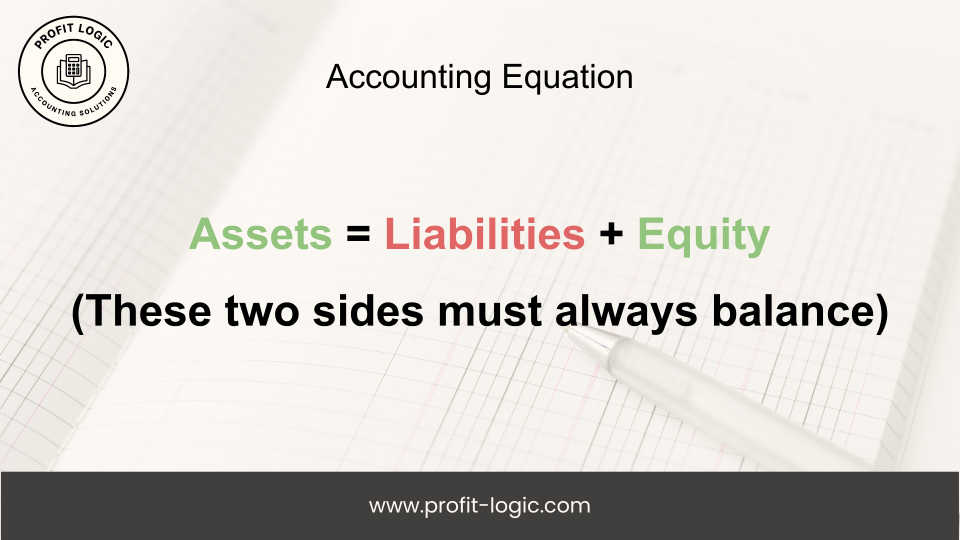

This system is governed by the accounting equation:

Assets = Liabilities + Equity

The accounting equation

Assets are what your business owns, such as cash, equipment, inventory, and money owed to you by customers. Liabilities are what your business owes to others, such as loans, credit cards, and unpaid bills. Equity represents the owner’s financial interest in the business.

The rule is simple but absolute: both sides of the equation must always balance. Every transaction must keep this equation in equilibrium. While this may look intimidating at first, you do not need to calculate it manually. Bookkeeping software handles the math—but only if transactions are categorized correctly.

Understanding this equation explains why careless categorization causes problems. If you label transactions based on guesses rather than principles, the software will still balance—but the story it tells will be misleading.

Understanding Assets, Liabilities, and Equity in Plain Language

Assets represent value controlled by the business. This includes cash in bank accounts, inventory held for sale, equipment, and money owed to you by customers.

Liabilities represent obligations. These include credit cards, loans, unpaid vendor bills, and taxes owed but not yet paid.

Equity often causes confusion. In simple terms, equity represents the owner’s claim on the business. It includes money the owner contributes, money the owner withdraws, and accumulated profits or losses over time.

When you invest money into your business, assets increase and equity increases. When you take out a loan, assets increase and liabilities increase. When you withdraw money for personal use, assets decrease and equity decreases.

Seeing transactions through this lens makes bookkeeping far more intuitive.

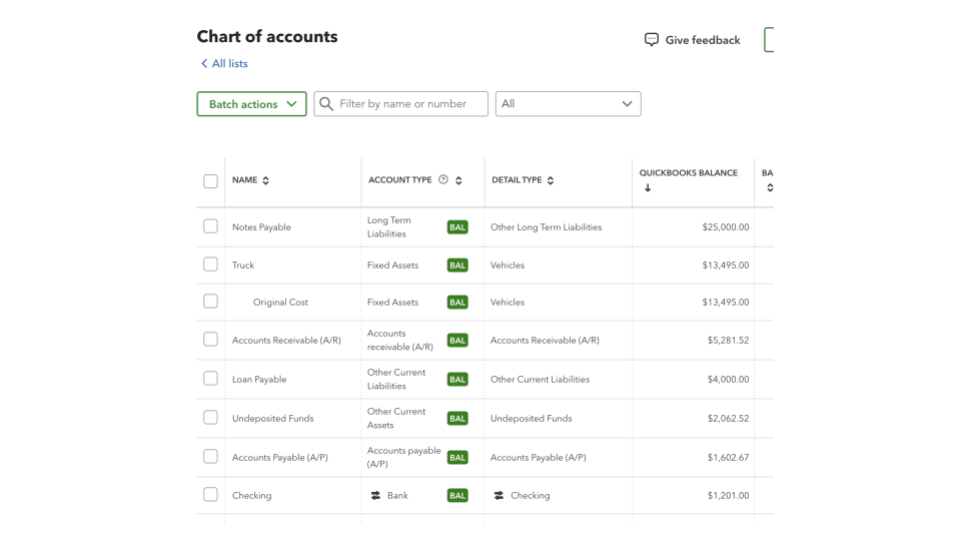

The Chart of Accounts: The Architecture of Your Bookkeeping System

Every bookkeeping system relies on a chart of accounts. This is a structured list of all the accounts your business uses to track financial activity. Each account falls into one of five categories: assets, liabilities, equity, income, or expenses.

The chart of accounts determines how transactions flow into your financial statements. Income and expense accounts feed into the Profit and Loss statement. Asset, liability, and equity accounts feed into the Balance Sheet. Together, they shape the Statement of Cash Flows.

Different businesses will have different charts of accounts depending on industry, size, and reporting needs. A consultant may need far fewer accounts than a retailer or contractor. There is flexibility here, but the structure must be intentional.

Think of the chart of accounts as the skeleton of your bookkeeping system. If it is poorly designed, everything built on top of it becomes harder to understand.

Categorizing Transactions: The Heart of Bookkeeping

Categorizing transactions is the most fundamental bookkeeping task and typically makes up the majority of ongoing work. Every time money moves in or out of your business, that transaction must be categorized correctly.

While there may be hundreds of possible categories, most transactions fall into a small number of common types.

Income represents money earned through products or services.

Expenses represent costs incurred to operate the business.

Transfers move money between accounts without affecting profitability.

Liabilities represent borrowed or owed funds.

Owner contributions and distributions reflect money moving between the owner and the business.

Example Bookkeeping Transactions (with Correct Classification)

1. You receive a $5,000 loan from a bank to start your business.

This is a liability.

Your cash increases, but you now owe that money back to the bank.

2. You pay to advertise your business in a newspaper or online platform.

This is an expense.

The cost reduces your profit for the period.

3. You complete work for a client, but they have not paid you yet.

This is still income, recorded as an asset (accounts receivable).

You earned the money even though the cash has not hit your bank account yet.

4. You transfer money from your business PayPal account to your business checking account.

This is a transfer.

No income or expense is created—money is simply moving between accounts.

5. You purchase a personal item for yourself using your business credit card.

This is an owner distribution, not an expense.

The business paid on your behalf, reducing your equity in the business.

Understanding these categories prevents common errors. For example, purchasing a personal item with a business credit card is not an expense—it is an owner distribution. Mislabeling this type of transaction distorts profitability and creates tax issues.

This is why bookkeeping is not just data entry. It requires judgment grounded in accounting principles.

Bank Reconciliation: The Quality Control Step Most People Skip

Bookkeeping is recordkeeping, which means it must be verified. Bank reconciliation is the process of comparing the transactions recorded in your bookkeeping software with your actual bank and credit card statements.

Reconciliation ensures that nothing is missing, duplicated, or recorded incorrectly. It is similar to checking your work against an answer key.

Reconciliations are typically performed monthly for checking accounts, savings accounts, and credit cards. The goal is to match the ending balance in your software to the ending balance on the bank statement. If the numbers do not match, you investigate until they do.

Skipping reconciliation is one of the most common DIY bookkeeping mistakes. Without it, errors can accumulate silently and undermine your financial reports.

The Three Financial Reports Every Business Owner Should Know

Bookkeeping exists to produce financial reports. There are three core reports every business owner should understand.

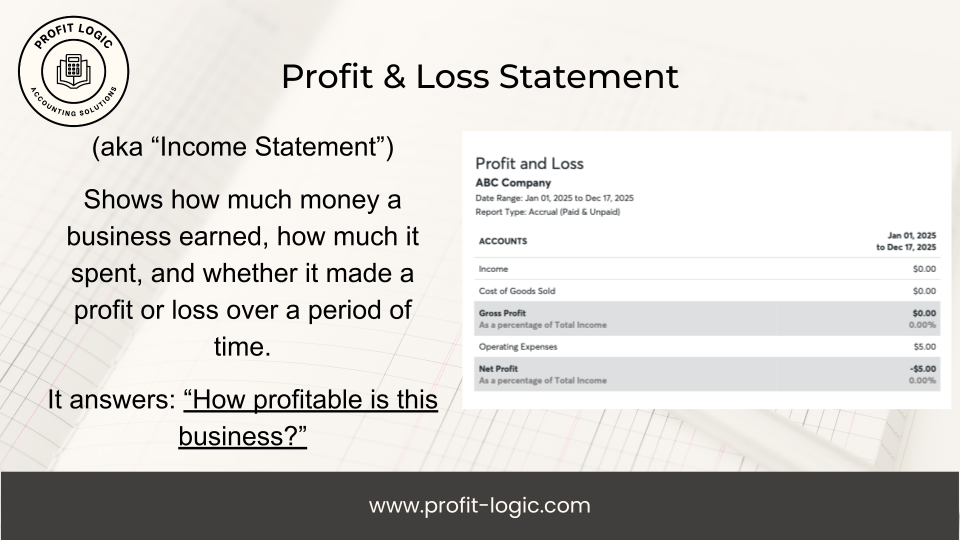

The Profit and Loss Statement shows income, expenses, and net profit over a period of time. It answers the question: How profitable is the business?

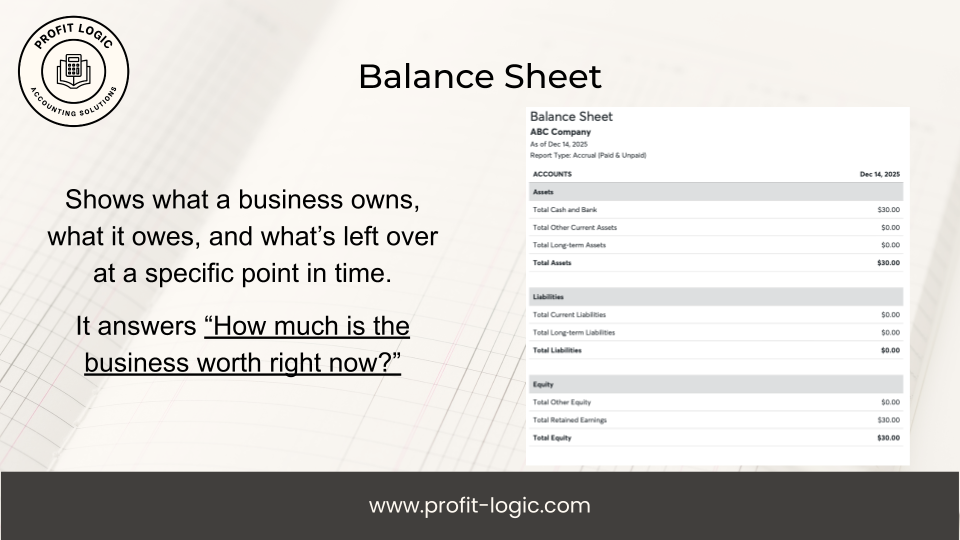

The Balance Sheet shows what the business owns, what it owes, and the owner’s equity at a specific point in time. It answers: What is the business worth right now?

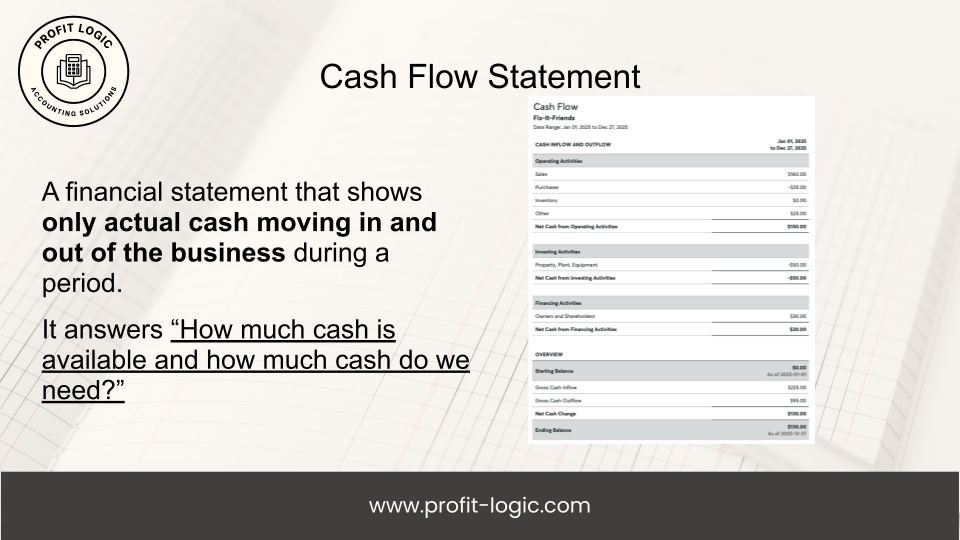

The Statement of Cash Flows shows how cash moves in and out of the business. It explains why a business can be profitable on paper but still struggle with cash.

If these reports are inaccurate, every decision built on them becomes riskier than it needs to be.

Building a Sustainable Bookkeeping Routine

Consistency matters more than perfection. A simple routine prevents small issues from becoming major problems.

Many businesses benefit from weekly transaction categorization. This keeps information fresh and reduces detective work later.

Monthly reconciliations and financial reporting should follow once bank statements are available. Reviewing your Profit and Loss statement monthly helps you stay connected to your business performance.

More complex analysis can be done quarterly or annually depending on your goals.

Choosing Between QuickBooks, Wave, and Other Tools

Most modern bookkeeping is done using software. QuickBooks remains the industry standard due to its robustness and widespread support, though it comes with a learning curve and higher cost.

You can check out QuickBooks here

Wave is a strong option for smaller businesses and solopreneurs. It is more affordable and easier to use, but less suited for inventory‑heavy or complex operations.

You can check out Wave here

Spreadsheets alone are rarely sufficient beyond very small side businesses. They lack safeguards, audit trails, and automated reporting.

The best tool is the one that matches your business needs and is used correctly.

DIY Bookkeeping vs. Hiring a Professional

Some business owners manage their own books, while others hire professionals. Both approaches can work depending on complexity, time, and comfort level.

DIY bookkeeping requires learning both accounting fundamentals and software workflows. Guesswork increases risk.

A quality bookkeeper should understand accounting principles, reconcile accounts regularly, communicate consistently, and provide reliable reports.

If you are unsure which path is right for you, a discovery call can help clarify whether DIY bookkeeping, cleanup work, or ongoing support makes the most sense.

When to Get Help—and What to Look For

If bookkeeping feels overwhelming, consumes too much time, or creates anxiety, it may be time to get help. A good bookkeeper provides clarity, not confusion.

Look for someone with demonstrated accounting knowledge, relevant experience, strong communication, and consistent processes. Cheap bookkeeping often becomes expensive later through cleanup and corrections.

Next Steps: Learning, Support, and Clarity

If you want a guided walkthrough of these concepts, I recommend watching the full Bookkeeping 101 webinar, where I explain these ideas visually and step by step.

If you want personalized guidance, help cleaning up your books, or ongoing bookkeeping support, you are welcome to schedule a discovery call through Profit Logic Accounting. We can discuss your business, your goals, and the level of support that makes sense for you.

Bookkeeping does not need to be intimidating. With the right foundation and support, it becomes a tool for clarity, confidence, and better decision‑making.

Ready to stop guessing and start trusting your numbers?

Your business deserves financial information you can trust.